VC Angle Weekly Briefing #26: Brussels Might Weaken GDPR for AI & EU Launches €5BN Scale-Up Fund

VC Angle Weekly Update #26

Hey - welcome to the twenty-sixth edition of VC Angle Weekly Updates! As always, we're keeping tabs on what actually matters across 🇪🇺 European tech. If something broke the news this week and it's worth your time, it's probably below. Scroll on for the deals, roles, reads, and events you'll want on your radar.

In This Edition:

Brussels trades privacy for AI competitiveness

Lovable nears 8M users, traffic down 40%

Denmark backs TechBBQ with €800k

EU finalizes €5bn Scale-Up Fund

Europeans are obsessed with Americans. Americans don’t care

VC investor predicts 40-50% fund consolidation

📰 What Happened This Week

The European Commission’s leaked “Digital Omnibus” package, set for November 19 release, would weaken core GDPR protections to accelerate AI development. The proposal allows companies to process personal data—including sensitive health and political information—for AI training under vague “legitimate interest” exceptions, while shifting cookie consent from opt-in to opt-out.

Privacy advocates like Max Schrems call it a “poorly drafted quick shot” that bypasses proper lawmaking procedures, with opposition from France, Austria, Estonia, and Slovenia, though Germany surprisingly backs the changes.

Lovable nears 8M users while questions about vibe coding sustainability linger

Stockholm’s Lovable hit 8 million users in its first year, tripling from July’s 2.3 million, with 100,000 products built daily on the platform. The $1.8 billion-valued AI coding startup hit $100 million ARR in June, but Barclays data showed traffic down 40% by September, raising questions about whether the vibe coding boom has staying power beyond the initial hype cycle.

TechBBQ received a €800k grant from Denmark’s Business Development Board, the second this year, as part of a larger 122M DKK investment round. The 2025 summit drew 10,000 participants including 3,500 startups and 1,700 investors, with the funding aimed at strengthening Denmark’s startup ecosystem and maintaining Copenhagen’s position as a major European entrepreneurship hub.

EU finalizing €5bn Scale-Up Fund for AI, quantum, and semiconductors

The European Union is setting up a €5bn Scale-Up Europe Fund targeting late-stage rounds above €100m in strategic tech sectors. The fund already secured €3bn in commitments plus €1bn from the European Innovation Council, with Denmark’s EIFO, Spain’s Criteria Caixa, and Novo Nordisk Foundation in talks to join. The European Commission eventually wants to expand it to €25bn, though Speedinvest’s Andreas Schwarzenbrunner called even €5bn “a good first step, but still tiny compared to what’s happening globally.”

🔍 Reads & Reports

Europeans obsess over America, but Americans don’t think about Europe at all

Index Ventures published Winning in the US, a data-driven guide for European and Israeli companies entering America, based on studying hundreds of VC-backed expansions and interviews with 40+ founders including Nikolay Storonsky, Ilkka Paananen, and Daniel Ek.

The breakthrough: there’s no single path. Success depends on matching your archetype to your strategy. Get it wrong, and you might burn millions without getting where you’re heading.

The four archetypes:

Telescope - Marketing-led, US is large but not dominant market. Gaming companies (King, Supercell, Voodoo) can scale globally from Helsinki or Paris via app stores and performance marketing. Most teams just stay in Europe.

Magnet - Sales-driven, US is vast majority of market. Enterprise software and cybersecurity companies must move founders to US. CEO needs presence to close deals and clients that would actually use the product.

Pendulum - Truly balanced. US becomes ~half the business, but Europe remains important. Spotify and Celonis built significant teams on both continents. Founders literally split time 50/50.

Anchor - Europe remains dominant geography and largest market. US grows but stays smaller portion. This is common for fintech: Adyen, Revolut. Industries where you can build €100B+ company in Europe alone.

Index partner Martin Mignot’s key observation: Europeans obsess about American politics and markets. Americans barely think about Europe at all. This indifference means founders start from absolute zero—unknown and irrelevant until proven otherwise.

Max Bray argues the industry will bifurcate into massive platforms and specialist boutiques, with the middle basically disappearing by 2035.

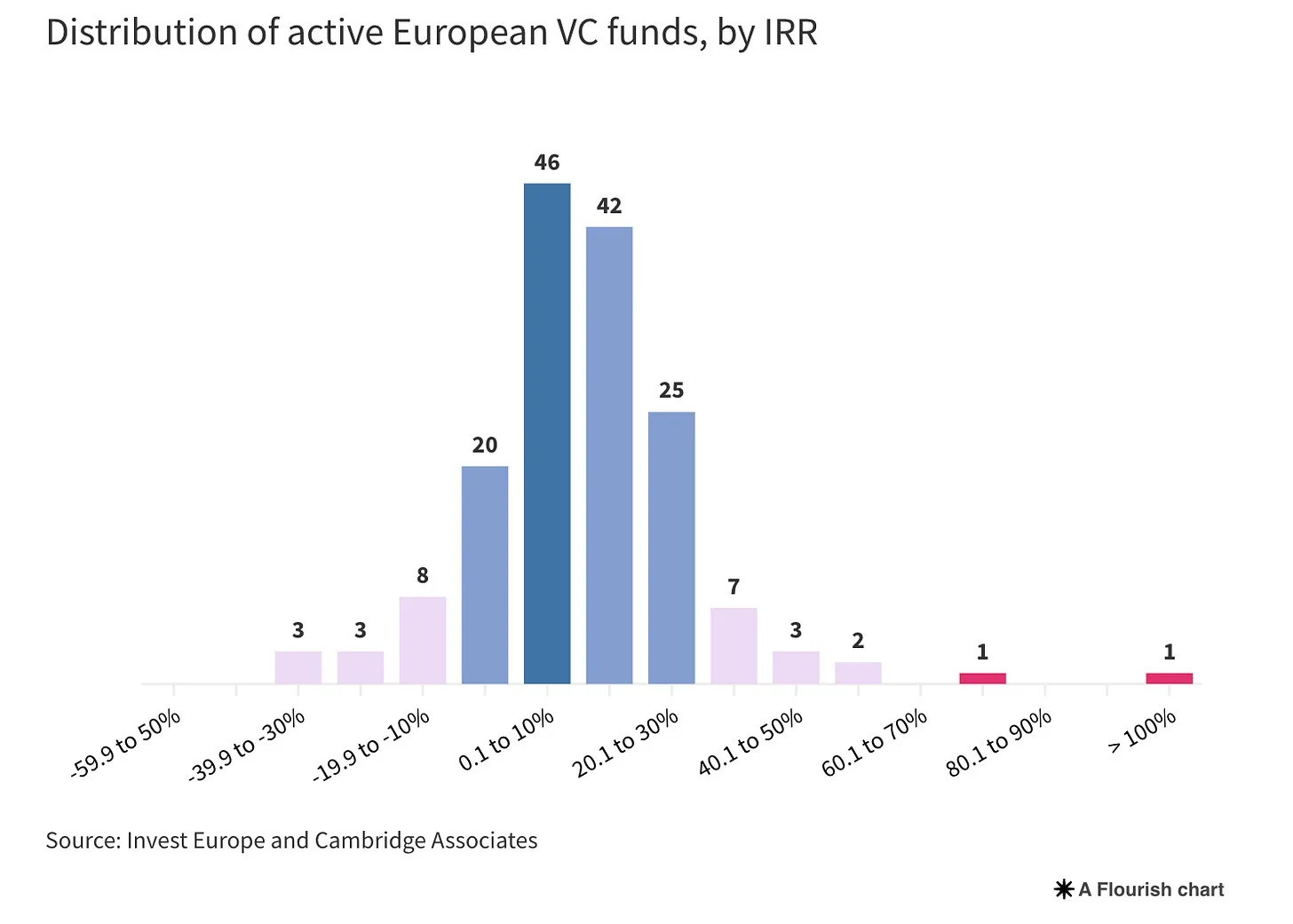

Venture barely beats public markets (European funds averaged 12.87% IRR vs S&P’s 10.48%), but 80% of European funds returned <10% IRR. Average time to 1x DPI is eight years, with real returns closer to 13 years. LPs question locking money in such illiquid assets.

The economics are as follows: 2,831 early-stage funds in Europe chase 13 unicorns per year—1:217 odds. Over five years, that’s 1:43 chance versus the 1:25 power law VCs claim. Just 30 firms raised 75% of all 2024 capital; 9 took 50%.

Software startups need less capital: AI increased output per employee, lowering headcount, a direct proxy for the amount of fundraise needed. Tools are available for everything, from incorporation to payroll reduced barriers. “Seed-strapping” and “minimum viable venture” have normalized as founders pursue profitability faster.

The prediction: mega-platforms like a16z raising $10B+ vehicles will function as hedge funds skimming management fees and influencing policy. Specialists will win through sector expertise and taste. Funds trapped at $200M-$1B—too big for boutique economics, too small for platform scale—face extinction.

💶 Where Funds Went (Or Will Go)

Startups

🇬🇧 Zilch → Raised $175M in equity and debt

🇩🇪 FMC → Raised €100M to launch a new class of AI-era memory chips.

🇨🇭 Delvitech → Raised $40M Series B to scale AI-powered inspection

🇨🇭 Acurast → Raised $11M to launch a smartphone-powered compute network.

🇮🇹 CommerceClarity → Completed €2.7M to power agentic e-commerce

🇫🇮 Cronvall → Secured €3.9M to digitise industrial procurement

🇩🇰 Arkyn → Raised €4M to grow its enterprise software suite.

🇩🇰 Skycore Semiconductors → Raised €5M to advance next-gen AI data-centre chips.

🇱🇹 Self.co → Raised €2.56M to expand molecular allergy testing.

🇫🇮 CHAOS → Attracted €2M to scale its real estate data intelligence platform.

🇩🇪 CERPRO → Secured ~€2M Pre-seed to modernise industrial quality assurance.

🇫🇷 Zaiffer → Launched with €2M backing from Zama and PyratzLabs to bring confidential computing to DeFi.

🇮🇸 Euler → Closed €2M Seed to scale AI-driven software for 3D printing.

🇬🇧 FALKIN → Secured $2M to protect bank customers from AI-driven scams.

🤝 M&A

🇧🇪 DataCamp → Acquired Dubai-based Optima to strengthen its AI education engine.

Investors

🇬🇧 Backed VC → Closed $100M Fund III.

🇫🇮 Vendep Capital → Raised €80M for its fourth fund.

🇩🇪 Oyster Bay → Closed €100M Fund II focused on food & biotech.

👋 That’s a wrap for this week.

If you’ve got a round, role, or resource others should see, reply to this or ping us at hello@patrons.vc or send me a message on LinkedIn. We’re building Europe’s finest scouting network at Patrons. If you have a good deal flow, want to expand yours, or want to reach the right investors, send us a message!

If you found this useful, send it to a founder or friend who’d appreciate it.

Couldn't agree more. That 'legitimate interest' loophole for AI data processing feels like a hilariously quick fix for a complex problem. Will it genuinely boost our tech scene, or just create more ethical headaches?