VC Angle Weekly Briefing #27: Slush Draws 13,000 participants & Europe's $132B AI Gap Widens

VC Angle Weekly Update #27

Hey - welcome to the twenty-seventh edition of VC Angle Weekly Updates! As always, we're keeping tabs on what actually matters across 🇪🇺 European tech. If something broke the news this week and it's worth your time, it's probably below. Scroll on for the deals, roles, reads, and events you'll want on your radar.

In This Edition:

13,000 at Slush, €4T represented

Big Tech delays EU AI rules

Europe’s largest defense-tech fund closes

70% of founders call Europe restrictive

Europe faces $132B AI funding gap

M&A becomes essential tool for European startups

📰 What Happened This Week

Slush 2025 draws 13,000 participants representing €4 trillion in startup-directed funds

Helsinki’s Slush 2025 attracted 13,000 participants including 6,000+ startup founders and fund managers representing over €4 trillion in funds directed to startups. Over 80% of participants came from European countries.

Lovable CEO Anton Osika opened the event, noting his company now sees 100,000 new projects built daily with 5 million people using Lovable-built apps. “Everyone kept telling me that to be successful I had to move to Silicon Valley. I resisted that and we kept the company in Stockholm, bringing talent from the US to work for us.”

Slush has become a founder factory: 15% of former Slush employees founded their own startups. Each international visitor spends an average €946 during the event, generating significant revenue for Finland’s economy. The Slush 100 competition offers funding directly from European VCs including General Catalyst and Cherry Ventures.

EU delays high-risk AI rules to 2027 after Big Tech pressure

The European Commission’s “Digital Omnibus” package delays stricter AI rules in high-risk areas to December 2027 from August 2026. Affected areas include AI use in biometric identification, job applications, exams, health services, creditworthiness, and law enforcement.

The package also allows Google, Meta, and OpenAI to use Europeans’ personal data to train AI models under revised GDPR provisions, and simplifies cookie consent rules.

Big Tech lobby CCIA (Amazon, Apple, Google, Uber) welcomed the delay but called for “bolder” actions. Privacy advocates condemned it. Max Schrems called it “the biggest attack on Europe’s digital rights in years.”

European Consumer Organisation BEUC director Agustín Reyna: “The Commission’s proposal can only be read as deregulation almost to the exclusive benefit of Big Tech.”

Keen Venture Partners closes Europe’s largest defense-tech VC fund at €150M+

Amsterdam-based Keen Venture Partners announced the first close of its European defense and security fund at over €150 million, making it the largest defense-tech VC fund in Europe.

Major backers include the European Investment Fund (€40 million), Dutch pension fund PME (€40 million), TNO, ABN AMRO, and LIOF. The fund plans to invest €1-€10 million in over 25 companies focusing on cybersecurity, autonomous systems, deterrence technologies, and space capabilities.

Context: EU defense spending hit €343 billion in 2024 (1.9% of GDP), projected to reach 2.1% in 2025. Other European defense funds include Rockaway Ventures’ €55 million second fund and Presto Tech Horizons targeting €150 million.

🔍 Reads & Reports

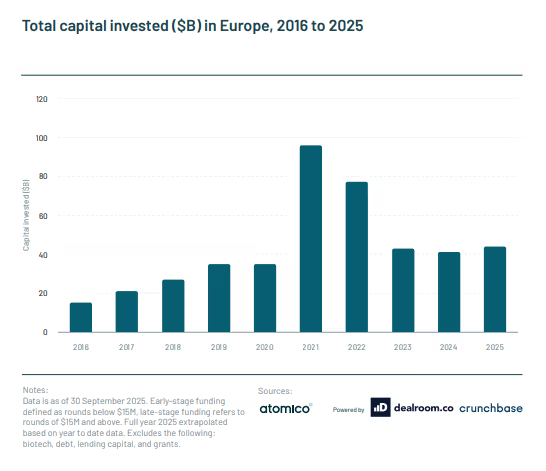

Atomico’s 280-page report projects European tech investment will reach $44 billion in 2025, with deeptech now capturing 36% of VC funding compared to 19% in 2021. Defense tech raised a record $1.6 billion this year, up 55% year-over-year, while France’s Mistral closed a €1.73 billion round.

The report identifies structural problems: 70% of founders find Europe’s operating environment too restrictive, European pension funds allocate 0.01% to VC versus 0.03% in the US, and 18% of European founders now incorporate in the US (up from 10% in 2016).

The capital gap is stark—Europe raised $14 billion for AI against $146 billion in the US. European Commission initiatives like the 28th Regime aim to address market fragmentation, but implementation is still uncertain (with it might ending up as a directive instead!) given past regulatory outcomes with GDPR and the AI Act.

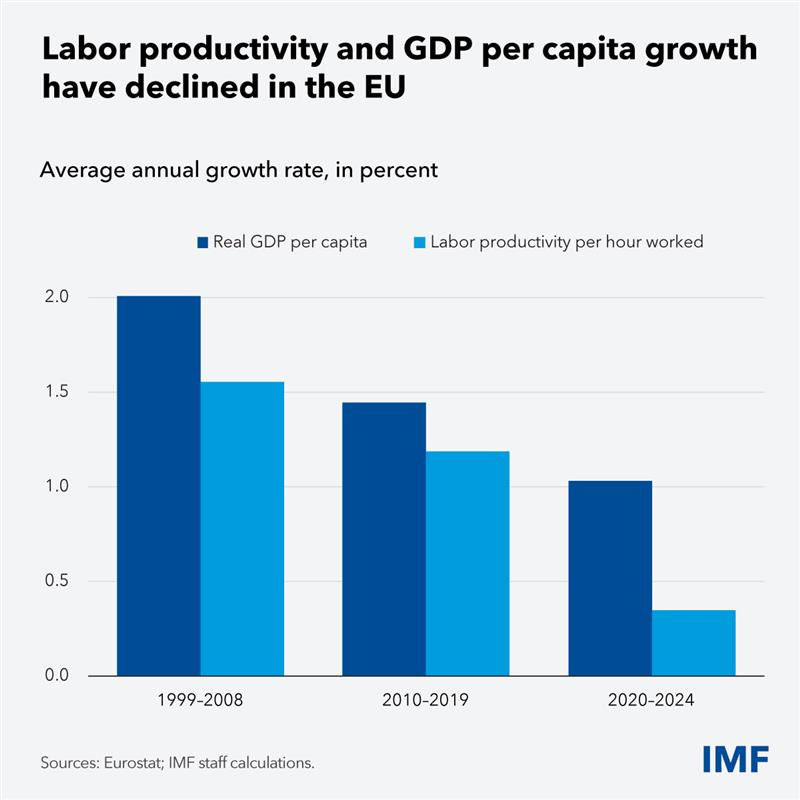

IMF research projects Europe will achieve 1.1% cumulative productivity growth over five years from AI adoption alone, with gains varying by country—Norway could reach 5% in an optimistic scenario while Romania stays below 2%. Higher-income European countries stand to benefit more because their economies have greater exposure to white-collar services where AI can automate tasks, and higher wages create stronger incentives to adopt labor-saving technology.

The IMF argues long-term gains could be substantially larger if AI accelerates R&D and creates new industries, though this requires policy action. The organization recommends deepening the EU single market to reduce cross-border barriers, strengthening Capital Markets Union to channel more venture capital to AI ventures. Without these reforms, even the modest near-term productivity gains could be lost.

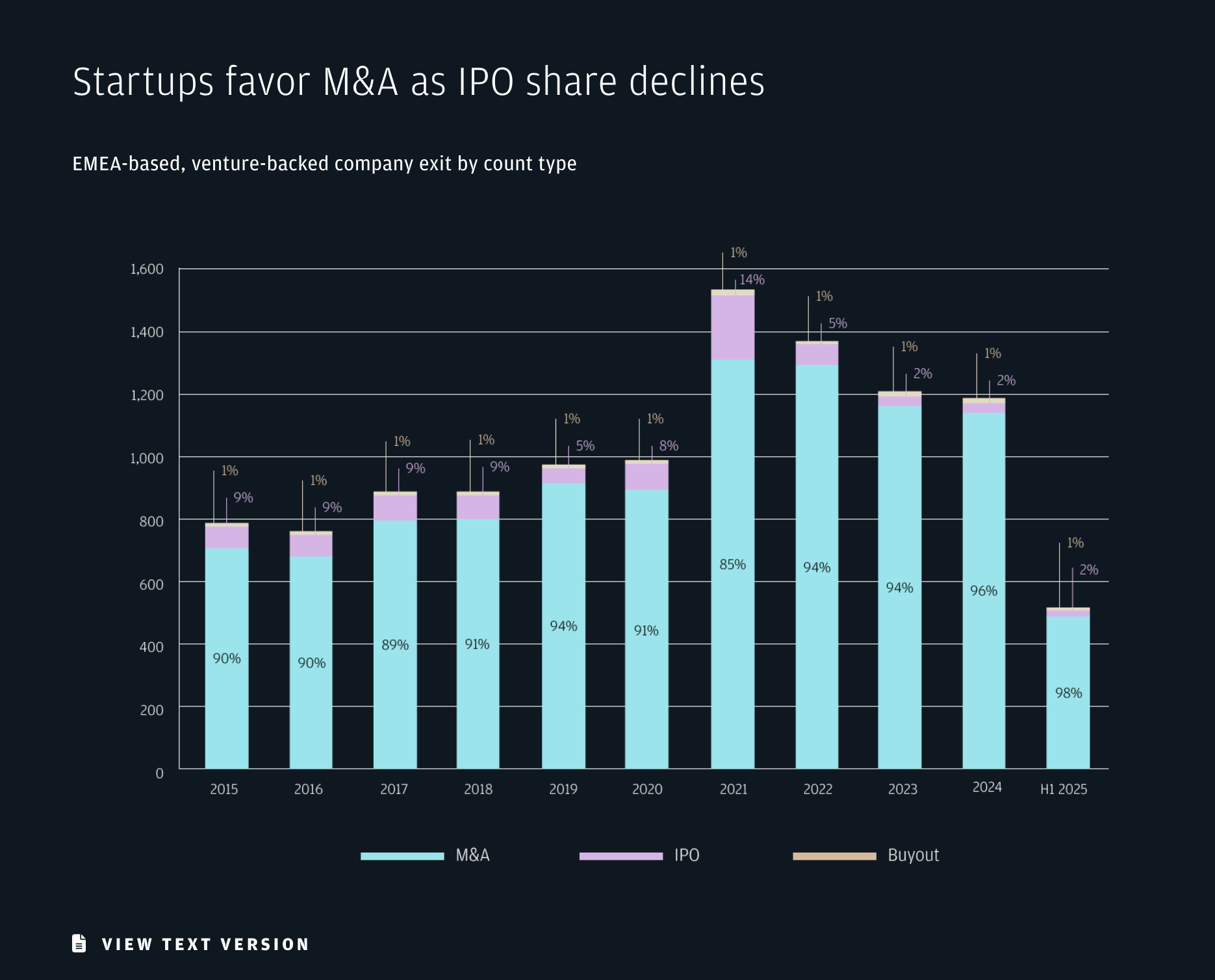

European startups abandon “buying growth” stigma as M&A becomes efficiency play

European founders historically avoided acquisition-led expansion, wary of being perceived as “buying growth.” That stigma has faded. The logic is now mechanical: (1) acquire competitors to reduce pricing pressure; (2) buy product capability to shorten development cycles; (3) absorb regional operators to skip market entry from zero, and (4) purchase teams to avoid recruitment.

Mergers and acquisitions account for over 85% of venture-backed exits across Europe over the past five years, with US-based acquirers leading deal flow. Both corporate and venture-backed buyers are increasingly active in the EMEA market as private equity begins rotating portfolio companies.

“LLMs are like as refrigeration. And the Coca-Cola has yet to be built”

“The people who invented refrigeration made some money, but most of the money was made by Coca-Cola, who used refrigeration to build an empire.”

💶 Where Funds Went (Or Will Go)

Startups

🇳🇱 Picnic → Raised €430M to scale its online grocery platform.

🇩🇰 Flatpay → Raised $170M and reached unicorn status

🇬🇧 Artios → Raised $115M Series D to accelerate cancer therapies.

🇩🇪 voize → Raised $50M Series A to bring AI to frontline nursing.

🇫🇷 Deblock → Secured €30M Series A to expand on-chain banking in Europe.

🇫🇷 GetVocal → Raised $26M to scale AI customer-support agents.

🇬🇧 BOB → Secured $25M to accelerate Bitcoin DeFi expansion.

🇷🇴 Condukt → Raised $10M to modernise compliance for financial services.

🇨🇭 Albatross → Raised €10.5M to expand real-time product-discovery AI.

🇩🇪 Peec AI → Raised $21M Series A to help brands win in AI search.

🇩🇪 Mirantus Health → Raised €5.5M to scale faster eye-screening diagnostics.

🇫🇷 NcodiN → Raised €16M to advance deeptech semiconductor innovation.

🤝 M&A

🇬🇧 Curve → Acquired by Lloyds to integrate multi-card fintech into banking services.

🇩🇪 Integral → Acquired cleverlohn while securing fresh funding for its AI accounting and payroll platform.

Investors

🇫🇮 EIT Urban Mobility → Launched a new €44M fund for mobility innovation.

🇬🇧 RCA → Closed its Design & Innovation S/EIS fund

🇪🇺 Sofinnova Partners → Secured €650M to back breakthroughs in biopharma and medtech.

👋 That’s a wrap for this week.

If you’ve got a round, role, or resource others should see, reply to this or ping us at hello@patrons.vc or send me a message on LinkedIn. We’re building Europe’s finest scouting network at Patrons. If you have a good deal flow, want to expand yours, or want to reach the right investors, send us a message!

If you found this useful, send it to a founder or friend who’d appreciate it.