Why Do Most VCs Follow Consensus?

Everyone wants to be contrarian, but most end up imitating them.

Sir Humphrey Appleby: Didn’t you read the Financial Times this morning?

Sir Desmond Glazebrook: Never do.

Sir Humphrey Appleby: Well, you’re a banker. Surely you read the Financial Times?

Sir Desmond Glazebrook: Can’t understand it. Full of economic theory.

Sir Humphrey Appleby: Why do you buy it?

Sir Desmond Glazebrook: Oh, you know, it’s part of the uniform. Took me thirty years to understand Keynes’ economics. Then when I’d just cottoned on, everyone started getting hooked on these new monetarist ideas, you know, “I Want To Be Free” by Milton Shulman.

Sir Humphrey Appleby: Milton Friedman.

Sir Desmond Glazebrook: Why are they all called Milton? Anyway, I’ve only got as far as Milton Keynes.

Sir Humphrey Appleby: Maynard Keynes.

Sir Desmond Glazebrook: I’m sure there’s a Milton Keynes.

Sir Humphrey Appleby: Yes, there is, but it’s...

[Humphrey gives up]

as chronicled in “Yes, Minister”, Series 2, Episode 6: "The Quality of Life":

TL;DR

John Maynard Keynes learned the hard way that markets do not reward objective truth as neatly as economists like to think. Prices move not just on facts, but on how people think other people will react to those facts. His “beauty contest” analogy captures the logic well: success comes not from picking what is best, but from picking what others will choose. Venture capital works the same way, often even more so than public markets. VCs may praise contrarianism, but most allocate based on lagging indicators: social proof, visible traction, brand-name co-investors, and categories the market already understands. That is not necessarily because they lack imagination, but because VC is shaped by incentives. The game is not only about returns, but also reputation and fundraising. In that structure, lagging indicators become rational: they help investors coordinate, reduce career risk, satisfy LPs, and mobilise networks. Venture may celebrate originality in theory, but in practice it often rewards what is already legible.

⏱️ 16:31 Est. Reading Time

The Beauty Contest of 1936

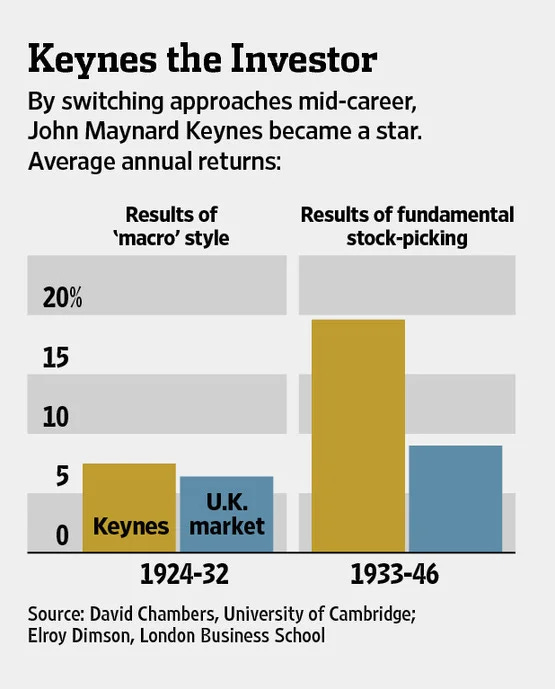

For a good while, one had thought that if the facts were clear, if the bigger (macro) picture was understood, and if one excelled at reading the forces shaping the economy better than anyone else, then good investing should follow. And if one was equipped for that kind of investing, it was him. The one in question is John Maynard Keynes, one of the great economic minds of his age, who then was managing an endowment fund for King’s College in Cambridge. Yet, the markets did not award brilliance in the way he expected. In his early years as an investor, his results were respectable at best. From 1924 until 1932, he only slightly outperformed a quite weak UK stock market, a particularity that made the lesson so severe. He undoubtedly had the intellect, information, and a command of macroeconomics that almost nobody on earth could match, and still the markets refused to behave.

So, he realised then, markets were not simply mechanisms for processing only facts, but also machines for processing human behaviour. Prices did not move because reality had been properly understood. They moved because people, in all their fear, greed, excitement, doubt, and imitation, decided to buy or sell. It was the conviction of the masses from the each side of the trade that carried the true force, not the “truth”. A phenomena he coined the term “animal spirits” for; by which he meant the emotional and psychological energy that drives human action, especially under uncertainty. Investors, prone to all the human vices, do not move in straight lines from facts to price.

Once Keynes comprehended this, his investing changed. After 1932, he moved away from trying to read the world mainly through grand macroeconomic conclusions and became far more interested in individual assets, in value, and above all in how other people were likely to judge value. He no longer treated the market as a machine that should eventually subjugate itself to the facts, but as a social game in which expectations about expectations matter more than the reality itself. His record after that point improved dramatically.

To explain this logic metaphorically, Keynes described the old newspaper beauty contests in which readers were asked to choose the prettiest faces from a large group of photographs. The winner was not the person who picked the faces they personally found the most beautiful. The winner was the one whose choices best matched the choices of the crowd. So, to invest well, you are not simply asking what an asset is worth (or what it could be worth), but you are also asking what others think it is worth (or what it could be worth), and how that chain of perception will turn into action.1

“It is not a case of choosing those (faces) which, to the best of one’s judgment, are really the prettiest, nor even those which average opinions genuinely thinks the prettiest. We have reached the third degree where we devote our intelligences to anticipating what average opinion expects the average opinion to be.”

John Maynard Keynes

The same analogy appears, even more clearly, in venture capital and other private markets. Despite venture capitalists being, undoubtedly, better informed and more skilled at allocating resources than the broad masses, they still need to pick the face they think others will choose, not the one they personally found the prettiest. Read: they are not in the game of funding companies with the strongest fundamentals, but the companies most likely to raise the next round, because that is what determines their markup and returns.

Even more so, you could argue that in public markets — where prices eventually do converge to fundamentals due to continuous price discovery, short selling, liquidity, and other factors — the beauty contest is somewhat temporary, while in venture there is no such corrective mechanism. Rounds are infrequent, there’s no shorting, valuations are set by a few negotiators in opaque negotiations, and that “price” is quite literally just whatever the last investor agreed to pay.

By now, one might conclude either that venture capitalists have failed to understand this, or that the industry is populated by semi-independent actors simply deferring to collective consensus. Both conclusions miss the point. Most VCs allocate based on lagging indicators not because they lack the ability to identify leading ones, but because the incentive architecture of venture capital makes backward-looking allocation the individually rational strategy across multiple reinforcing dimensions. The purpose of this article, however, is not to argue that independent thinkers in venture have the wrong strategy (probably the opposite), but to explain why most VCs are simply not structured to behave like them.

Table of Contents

1. Lagging Indicators

2. Consensus Bets Reduce Reputational Risk

3. Network Effects & Coordination Games

4. FOMO & Information Asymmetry

5. Waiting as a Strategy When Downside Is Convex

1. Lagging Indicators

Ever since Peter Thiel’s Zero to One was published in 2014, the venture world has been fascinated by contrarianism: the strategy of investing against prevailing market consensus, betting on unpopular or overlooked ideas that hold the potential for massive, non-linear returns.

It was a direct challenge to the dominant venture habit of pattern-matching, which is inherently backward-looking. Thiel’s point, one I fully agree with, was simple: there is no new Airbnb. There is no new Uber. Those companies did not become iconic by resembling what came before them, but by building something genuinely new.

And yet, despite paying tribute to originality in theory, venture still tends to reason through analogy. You hear it all the time: “This is Uber for X.” “This market looks like SaaS in 2012.” “She reminds me of a young [successful founder].” Every such judgment is, by definition, a comparison to something that has already happened. Pattern-matching can identify companies that resemble past winners. What it cannot reliably identify are the truly novel ones, which is where the outsized, infamous power-law returns tend to come from.

That is why some of the best seed investors are often thesis-driven rather than purely pattern-driven. They start with a structural shift, technical, regulatory, cultural, or behavioral, and then look for founders building into that shift before it becomes obvious. That is a leading-indicator framework. It tries to identify where the world is moving, rather than merely recognise what has already worked. In venture, by contrast, lagging indicators are the signals that appear only after a startup has already been partially de-risked by market validation, customer traction, institutional attention, or early adoption. If investors rely too heavily on those signals, they should, in theory, arrive too late to the real source of alpha.

So why, then, do most VCs still rely on lagging indicators?

2. Consensus Bets Reduce Reputational Risk

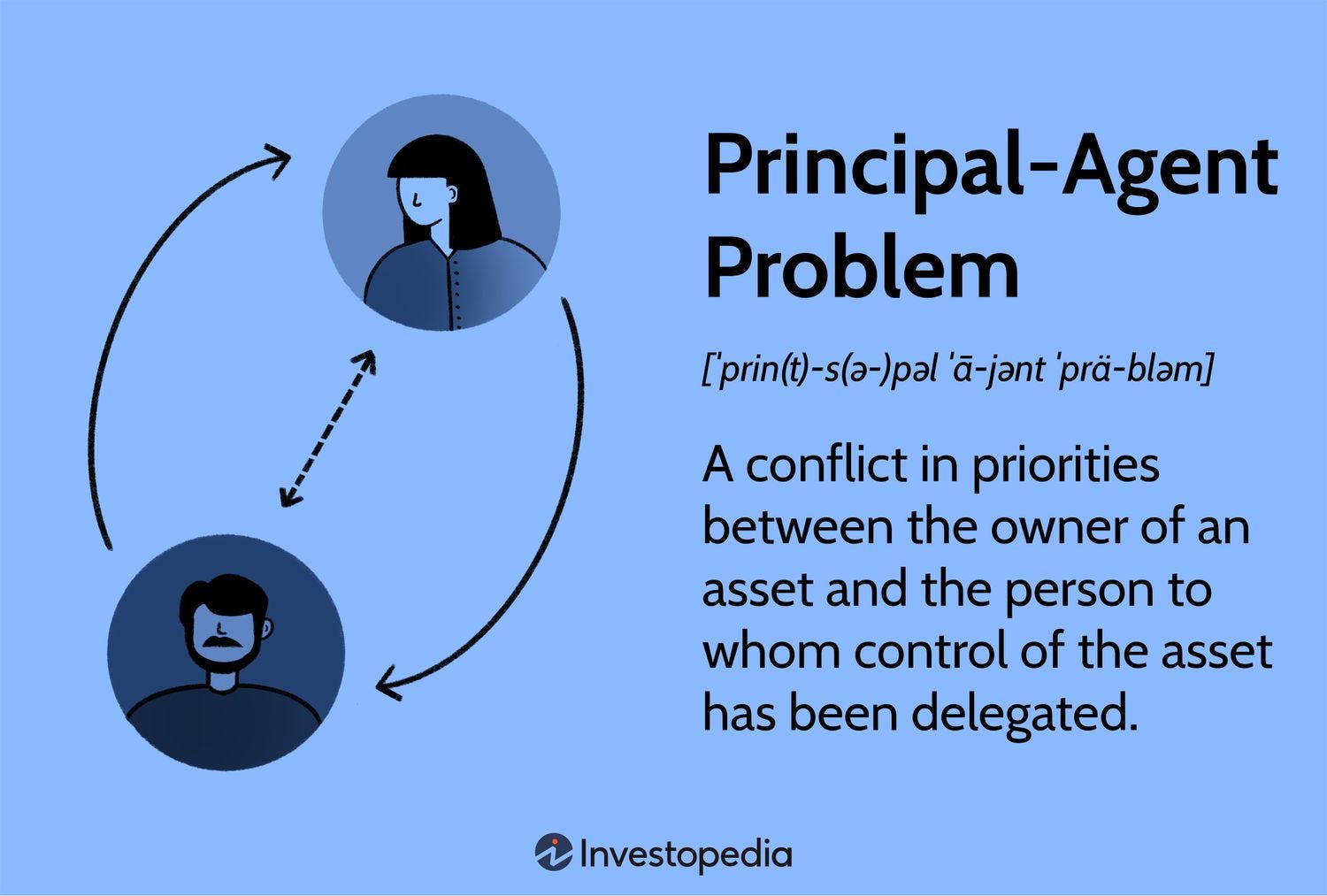

Despite what people often assume, venture capitalists arguably have one of the hardest tasks out there: they are paid to make judgments about a future that does not yet exist. But their job is not to predict the future in the abstract. Their job is to manage other people’s capital responsibly and generate credible returns over the life of a fund.

A VC then, as the agent, ends up optimizing for what the LP, as principal, can actually observe and evaluate:

recognisable co-investors

clean step-ups

visible market validation

exposure to categories the broader market already understands (i.e. consensus)

These are legible signals. They may not capture the deepest truth about a company, but they make an investment easier to explain, easier to defend, and easier to present as progress. The principal-agent structure of VC makes lagging indicators the rational choice for many individual partners. It creates asymmetric career risk: losing money on a consensus deal is survivable; losing money on an unconventional one is much harder to justify. Venture, after all, is now a highly institutionalised asset class. Once investing frameworks spread across the industry, sameness followed naturally. Everyone began looking at deals through roughly the same lens, tracking the same trends from the same data sources and platforms, and consuming the same intellectual diet. The result is predictable: people start thinking alike, and eventually investing alike.

And yet, despite data being increasingly commoditised and differentiated conviction mattering more than ever, relationship-based investing still works in hot markets, at least in the short term. Keynes’s logic applies here too. If enough credible investors believe others will continue to believe, the cycle sustains itself. Firms validate one another through participation, mark one another up across rounds, and if strong exits eventually materialise, the process can still be defended as sound stewardship of LP capital. In colder markets, however, it becomes a drag on performance, because venture is no longer rewarded for staying close to consensus, but for being right before consensus arrives. That is especially visible today outside the most crowded parts of software and the B2B AI application layer, where true conviction is needed to fund the technology of tomorrow (robotic, precision manufacturing, etc.).

But even when a VC knows that leading indicators matter more than lagging ones, the cost of acting on that knowledge is high. It requires speed, deep networks, serious technical diligence, and the conviction to take meaningful ownership before the market has made the company legible. Which brings us to the next major reason VCs largely follow lagging indicators.

“You ever wonder why fund managers can’t beat the S&P500? Because they’re sheep — and sheep get slaughtered! Most these Harvard MBA-types, they don’t add up to dog sh*t. Give me guys that are poor, smart and hungry — and no feelings.”

Gordon Gekko, “Wall Street” (1987)

3. Network Effects & Coordination Games

George Soros, much like Keynes before him, arrived at a similar conclusion: in reflexive systems2, beliefs shape prices. That runs directly against the standard economic models, such as the Efficient Market Hypothesis, which assume that prices merely reflect objective fundamentals and tend toward equilibrium. Soros, however, went a step further. He argued that beliefs do not just shape prices; prices then go on to shape fundamentals.

If, for example, investors believe a sector is growing, they buy in, driving prices up. Those higher valuations may allow companies to borrow more cheaply or issue new stock, which they use to fund further expansion. This “confirms” the initial bullish perception, attracting more buyers. What began as a perception starts to create the conditions that make the perception look true. The initial belief is reinforced by the consequences it produces, until the loop eventually breaks.

The same logic applies even more powerfully in private markets. A strong financing round is not just a reflection of quality; it can quite literally create quality. It gives a company more resources, more credibility, more hiring power, more customer trust, and more strategic room to execute. In that sense, belief shapes price, price shapes fundamentals, and the act of raising a strong round can make the company better at becoming what investors already hoped it was.

Most financing decisions are therefore made under strategic complementarity: your payoff improves if other credible investors also invest. If a respected founder, angel, or lead enters the deal, it is not only rational but efficient to infer that they have likely done serious work and diligence already. In these coordination games, “truth” matters less than common knowledge. What matters is not just whether something is good, but whether everyone knows that everyone else can see that it is good. A lagging indicator (or a consensus) is therefore valuable because it is publicly observable, so everyone can coordinate on it. Private leading indicators may be more insightful, but they do not help coordination if no one else can observe them.

Venture is also a repeated game. Sometimes a firm leads, prices the round, and takes the first reputational risk. Other times it follows, co-invests, or is pulled in through prior relationships. Those roles are not fixed; they change across cycles, and the network of firms depends on that constant rotation. From the outside, this can resemble simple crowding into the same deals. But much of what looks like imitation is really structure. Capital formation in venture is relational, and firms often move the way they do because the system rewards coordination as much as conviction. And beneath all of it sits venture’s deepest fear: not the error of commission, backing the wrong company, but the error of omission, missing the one that mattered.

4. FOMO & Information Asymmetry

Harry Stebbings recently shared that there are two particular deals he still loses sleep over years later:

ElevenLabs, where he passed on the chance to invest $250k in the Series A at a $100M post-money valuation. Three years later, ElevenLabs is already worth around $11B.

Deel, where he passed on the chance to invest $250k in the $12M seed round. Deel is now valued at $19B, costing Stebbings roughly $400M in potential gains and around $115M in personal carry.

Why does he after all these years still lose sleep over investment that he didn’t make and not all the deals that he invested in that failed?

Because venture is an asymmetric discipline. Its logic is unforgiving: missing a huge winner is far worse than backing an ordinary loser. A failed investment is part of the business. Missing the next Google, Uber, or Stripe can define how a fund, and sometimes a career, is remembered. In venture, what matters is not how often you are right, but whether you are present when the rare outlier appears. The game is driven by home runs. That is why following consensus can be a rational strategy. In any category cycle, whether AI, crypto, or climate, the entire market does not need to independently arrive at the same conclusion. It is often enough for a small number of high-status firms to move first with conviction3. Once they do, the rest of the market begins to reorganize around that signal, often without explicitly admitting that this is what is happening.

This is the logic of an information cascade. Each investor has some private signal, but they also observe the actions of others. When early movers act decisively, later investors infer that those firms must have seen something meaningful. Their own weaker or less certain signals then start to matter less. The observed behavior of credible early actors becomes the signal, as well as the fear of inadequacy of one’s own signal or analysis:

“Is there something that they know that I do not?”

Once the cascade begins, dissent becomes costly and often futile. In other words, it is rational to assume information asymmetry. This is yet again reinforced by venture’s power-law structure. The same firms repeatedly sit close to the most valuable companies. Over time, that track record itself becomes a source of authority. It would be naive to assume those firms have suddenly forgotten how to do their job. Other investors rationally assign weight to their behavior, and that weight helps propagate the cycle. The best leading indicators in early stage companes are rarely clean, public, or easily measurable. They are tacit, contextual, and often only visible to people with deep domain expertise or genuine proximity to the frontier. Most generalist funds lack both, so they default to public validation and the actions of investors assumed to know more than they do.

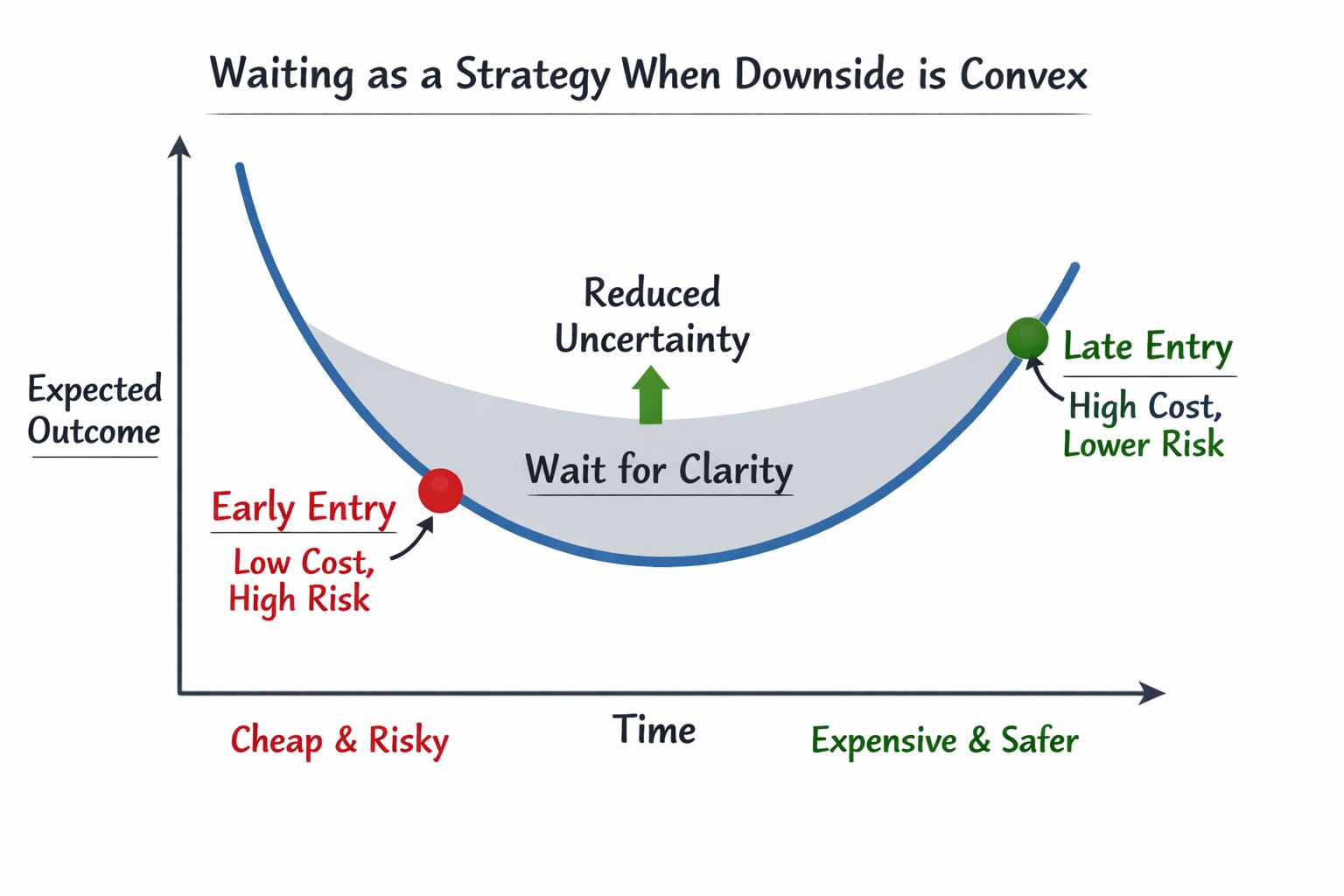

5. Waiting as a Strategy When Downside Is Convex

Private companies are staying private longer than ever. The path from founding to exit, whether through IPO or acquisition, now often stretches well beyond a decade. That changes the economics of timing in venture. For comparison, Amazon went public after roughly two years and Google after about five. Microsoft went public in 1986 at a valuation of around $350 million, or roughly $1 billion in today’s dollars. Today, its market capitalization is around $3 trillion. That means a majority of Microsoft’s value creation happened in public markets, not private ones4.

The implication is uncomfortable for venture capital. Early private investors in companies like Microsoft still did extremely well, but public-market investors who simply bought at the IPO and held on captured returns that, in some cases, rival or exceed the legendary outcomes of top venture deals. Accel’s Facebook investment, for example, is often cited as roughly a 1,000x outcome. Balderton’s early investment in Revolut has been estimated even higher on paper. But the broader point remains: when companies stay private longer, and when a large part of value creation is delayed or uncertain, the case for paying up later becomes more rational one would think at first.

This is where waiting starts to look less like hesitation and more like strategy. In real-options terms, many funds have the ability to invest later at a higher price but with far less uncertainty. Early entry means lower cost, but also far higher variance. Late entry means paying more, but for a company with a greater chance of survival, clearer product-market fit, stronger signals, and a more legible path forward. For funds with enough brand and access to enter those later rounds, that can be the better trade. In venture, being early and wrong means tying up capital in a company that may never raise again, may force a write-down, and may leave you defending a decision that the market never validated. Being later and right usually hurts far less. You pay more, but you buy a much higher probability that the company will survive, attract the next round, and keep compounding.

…And

VC is a game with three payoffs: (1) returns, (2) reputation, and (3) fundraising. Lagging indicators become the equilibrium strategy because they enable coordination, reduce reputational downside in a repeated game, provide auditable signals for principals, and increase positive externalities by mobilizing the network.

That does not necessarily make them optimal for finding the best companies earliest. It makes them rational within the structure most VCs actually operate in. The point is not that investors fail to understand leading indicators, but that the system often rewards what is legible, defensible, and easy for others to coordinate around.

“I can calculate the motion of heavenly bodies, but not the madness of people.”

Isaac Newton, reportedly after losing a fortune in the South Sea Bubble of 1720.

Similar phenomena has been studied in other experiments, such as the “Guess 2/3 of the average”.

According to George Soros, reflexive systems are dynamic, two-way feedback loops where participants’ subjective views (cognitive function) influence objective, underlying market realities (manipulative function), which in turn shape future perceptions.

That’s the “Leeds University experiment”. Researchers told 200 volunteers to randomly walk around a large hall without talking to each other. A select few were given detailed instructions on where to walk. They found that it only takes 5% of confident-looking, instructed people to influence the direction of the other 95%, and the volunteers did this without even realizing it.