The 60+ Companies Shaping Europe’s Security: Defence Database

Defence tech is the fastest growing tech sector in Europe, growing over 150% YoY in 2025. Here's what came out of it.

Dear friends,

Peter Thiel once noted how 4 out of 6 PayPal founders used to make explosives in their childhoods. Not entirely sure how they came around to that topic, but unlucky for them, they were born a few decades too early. The resurrection of defence tech arrived long after they'd settled for building PayPal.

Jokes aside, geopolitical upheavals, Russo-Ukrainian war, and a broader sense of unpredictability among policymakers, militaries, and investors changed what’s considered urgent and did so particularly in defence tech. Defence as a sector barely existed in Europe only 7-8 years ago, at least for VCs, but it’s fascinating to follow how quickly it exploded and what came out of it.

What I find particularly interesting about defence tech sector, beyond the geopolitics and power-games, is how many modern consumer technologies were originally adopted by defence before they got diffused to broader populace. GPS, internet, digital photography, microwave, touchscreens, Siri, and even duct tape and super glue were all originally adopted and used by the military forces first. You could say incredible things get invented when you require speed, possess budget, and have a moral mandate to replace humans in places where dying is a job description.

So when I look at the modern defence tech, building battlefield AI, autonomous drones, low-cost interceptors, GPS-denied navigation, quantum sensing, synthetic-aperture radar satellites, mixed-reality situational awareness for armoured vehicles, I also can’t resist thinking of what civilian technology will absorb over the next twenty to forty years. Could something from Helsing or ICEYE end up in my pocket in 25 years?

European Defence Tech Database

We couldn’t sit still until we find out, which is why we felt urged to compile European Defence Tech database. We kicked it off with 60 startups we considered the most promising at the minute, but we expect to keep the database live and add many others as suggestions and recommendations come in.

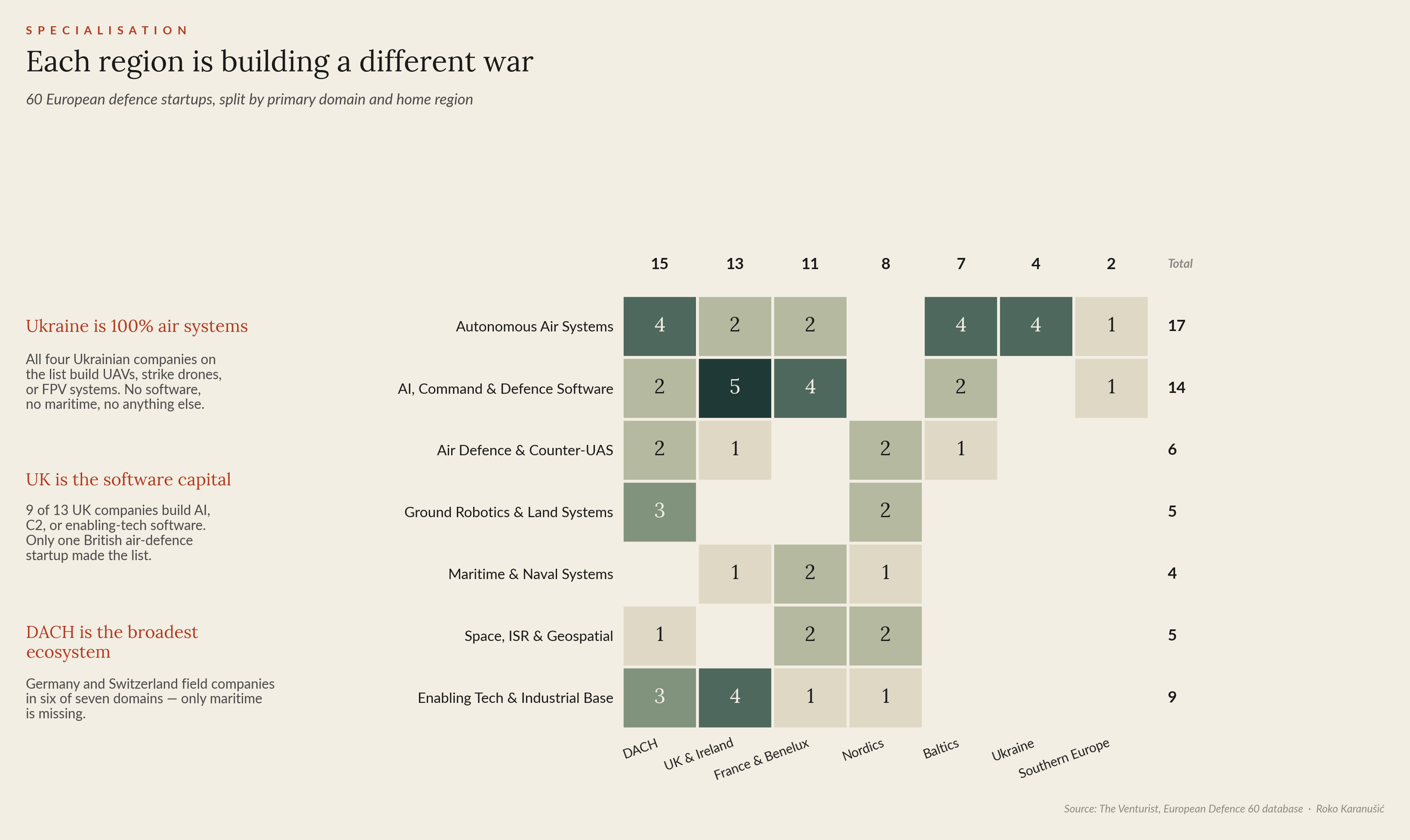

We've split the sixty companies into seven domains, by their primary product line: (1) autonomous air systems, (2) AI, command & defence software, (3) air defence and counter-UAS, (4) ground robotics and land systems, (5) maritime and naval systems, (6) space, ISR and geospatial, and (7) the enabling industrial base, meaning manufacturing, procurement, comms, energetics.

The full live database brings you the following:

Startup websites and LinkedIn URLs

Accurate descriptions of their main activities

Founding team

Founding year

HQ cities and countries

Notable institutional backers

Tags for easier search.

About the Europe’s Defence 60

It is, of course, naive to expect from a dataset of this size to produce perfectly accurate conclusions for the broader market, but there are certain trends that we can start observing already now.

A few takeaways made themselves clear:

Specialties: how each region has developed their own strengths, and it makes perfect sense

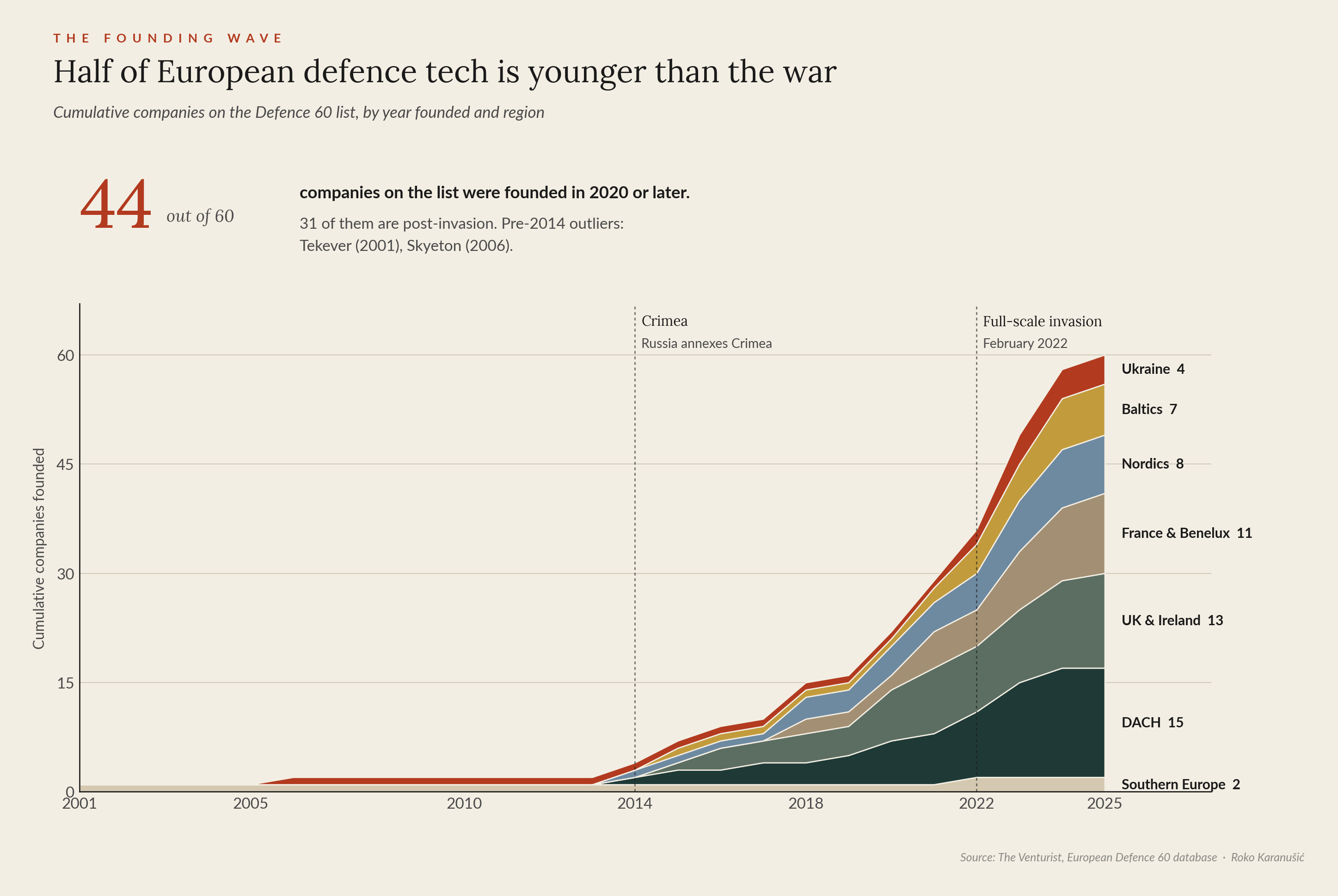

Youth: how ridiculously nascent the market is

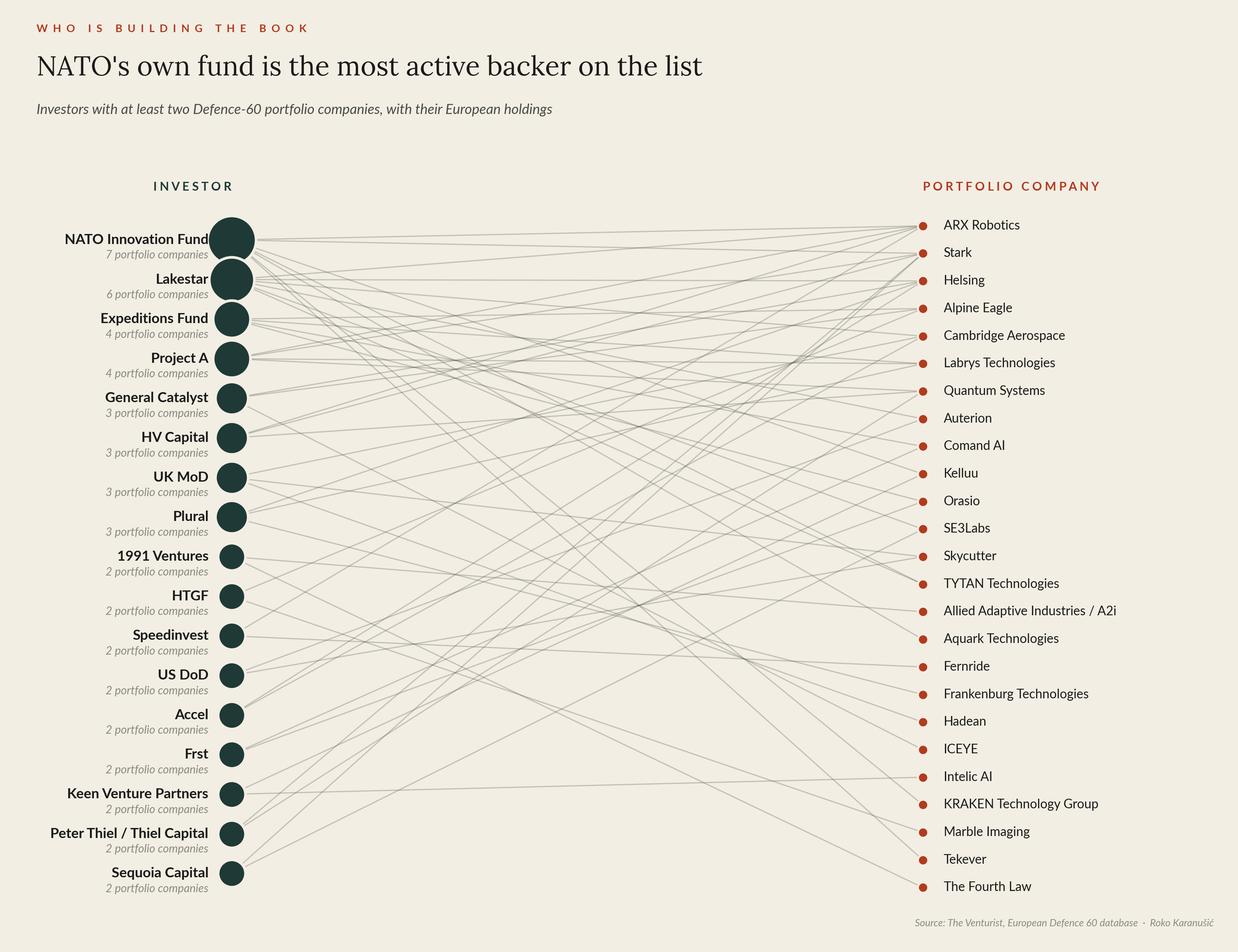

Government roles as backers: NATO innovation fund is leading the list of notable backers, backing 12% of all companies in the database. NATO innovation fund’s LPs are 24 NATO governments. Mind you, this fund was launched only in 2022.

Regional data

All 4 Ukrainian startups on the list (we counted Trypillian as British, even though it’s based in both London and Kyiv) are concerned with autonomous-air-systems. Buntar Aerospace, Skyeton, Terminal Autonomy, and The Fourth Law build UAVs, long-range strike drones, or FPV platforms. The result of the immense pressure of their circumstances made Ukrainian engineers extraordinarily good at making drones cheap, fast, and resilient under EW.

The UK is more proficient in command-software matters, enabling-tech and industrial base. 9 out of 13 British companies on the list build AI, C2, command-software, or enabling-tech/industrial base: Adarga, Arondite, Aquark, Hadean, Labrys Technologies, Vizgard, Delian Alliance (although this one spans categories), Allied Adaptive Industries and Rowden. It seems London has skilfully transplanted its fintech-style approach into defence: advanced data, decision support, and “Defence Finance Zig-Zag” secondments. Cambridge Aerospace is the lone British air-defence startup on the list, and KRAKEN Technology Group is the lone British maritime entry.

DACH is the most diverse base in Europe, missing only one category. They have contenders in every other category, with Germany alone having companies across six of the seven domains: air systems (Quantum Systems, Stark, Donaustahl), software, or software-enabled hardware (Helsing, Marble Imaging, SE3Labs), air defence (Alpine Eagle, TYTAN Technologies), ground robotics (ARX Robotics, Fernride, Swarm Biotactics), space and quantum (Munich Quantum Instruments), and enabling tech (3YOURMIND, GovRadar). Switzerland adds Auterion (although now based in Virginia) to the air-systems column. Of course, some startups, like Helsing, belong to multiple domains, but for the sake of categorisation we grouped them in their primary calling. The only domain missing from DACH is maritime, which makes intuitive sense given the geography.

Timing data

Excluding southern Europe with outlier data, the UK is the most established ecosystem here, with the median founding year of 2020. France and Benelux is the youngest one, at 2023. Those 3 years in venture could encapsulate a period from a seed round to Series B round, roughly speaking.

The UK and DACH waves started slightly earlier, between 2015 and 2020. Adarga (2016), Quantum Systems (2015), Hadean (2015), Rowden (2016), 3YOURMIND (2014) and Auterion (2017) were all founded well before the invasion occured. The Nordics similarly boast ICEYE, founded in 2014, Autoagri in 2018, Kelluu in 2018, and then a clean post-2022 acceleration with Nordic Air Defence, BlinkTroll Robotics, Sweden Ballistics and Crown Defence. Finland and Sweden had a head start in dual-use space and ISR, then layered air-defence and energetics on top once Russia redrew the priorities.

The Baltic and Ukrainian waves are almost entirely post-invasion. 71% of Baltic companies and 75% of Ukrainian companies on this list were founded in 2022 or later, the two highest post-2022 shares of any region. These two are possibly the most reactive and adaptive ecosystems right now.

Notable backers data

Seventeen investors on this list hold positions in at least two of the sixty companies. The most active, or say successful, is the NATO Innovation Fund, with seven portfolio companies: Aquark Technologies, ARX Robotics, Kelluu, Stark, Tekever, TYTAN Technologies and KRAKEN Technology Group. NATO Diana, a sister entity accelerator, also has a few involvements. The fund was launched explicitly to back dual-use technologies critical to allied security, and four years in, it is already the most concentrated investor in the category. For what is, in effect, multilateral sovereign capital, that is a great result.

Interestingly, and as one could expect considering the strategic importance of the sector, mission-aligned capital — NATO IF, EU defence vehicles, national MoDs, EUDIS, EIFO, Bpifrance, Definvest — appears in the cap tables of around 40% of the companies on this list.

The next tier reads: Lakestar, whose founder Klaus Hommels is also an appointed chair of the NATO Innovation Fund board, has 6 holdings (Auterion, ARX Robotics, Cambridge Aerospace, Helsing, SE3Labs, TYTAN Technologies), Expeditions Fund (4 — Labrys, Comand AI, Alpine Eagle, Orasio), Project A (4 — ARX Robotics, Labrys, Quantum Systems, Stark). Then a cluster at three holdings each — General Catalyst, HV Capital, UK MoD and Plural — and a long tail of two-holding investors including 1991 Ventures, HTGF, Speedinvest, US Department of Defense, Accel, Frst, Keen Venture Partners, Peter Thiel / Thiel Capital and Sequoia Capital.

Our Favourites

Sixty companies in one post are unfortunately too many to do justice to. Out of the database, three caught our attention more than the rest. Full-stack-AI-enabled precision mass and autonomous systems across all domains, cyborg insects, and cold-atom quantum systems; sounds like eschatology coming straight from the Book of Revelations. Here’s who they are and why we love them:

Helsing

AI-enabled precision mass for European defence

Website: https://helsing.ai/

Founders & leadership: Gundbert Scherf, Niklas Köhler, Torsten Reil

Tags: AI; autonomy; drones; defence software

YoF: 2021

Based in: Munich, Germany

Notable backers: Prima Materia (Daniel Ek), Lightspeed Ventures, Accel, Plural, General Catalyst, Saab, BDT & MSD Partners, Lakestar

What Helsing does

Helsing began as the unfashionable bet that battlefield AI would be a software problem. Köhler had spent years on deep learning at his earlier company Hellsicht, while Reil’s motivation, by his own account, came from watching Russia annex Crimea in 2014. They started in 2021 as a pure software company writing AI for the platforms that already exist, integrating into Eurofighter Typhoons, Saab Gripens, and Bundeswehr armoured vehicles.

Five years later, the software company makes drones and has moved far beyond software, describing themselves as building “AI-enabled precision mass and autonomous systems across all domains”. The HX-2, a 12-kilogram loitering munition with a hundred-kilometre range, navigates and targets without GPS using onboard AI and stored map data; Ukraine has it on the front line and Germany has signed a seven-year framework worth up to €1.46 billion.

As of May 11, 2026, they are reportedly in advanced talks to raise $1.2 billion at a staggering $18 billion valuation, led by Dragoneer and Lightspeed.

Why it is fascinating

The most consequential European defence company of this generation. It is one of the few European defence startups with credible ambition to become a full-stack prime: Helsing has gone from software vendor to drone manufacturer to fighter-jet AI to combat-aircraft builder in only five years.

Daniel Ek is the most unusual chairman in defence. The Spotify founder led the €100 million seed through Prima Materia in November 2021, has continued to lead subsequent rounds, and chairs the company. A consumer-internet founder anchoring a continent’s defence-AI flagship is just the most brilliant combo.

Software to hardware expansion is further strengthening the moats. When the AI and the airframe are designed together, performance characteristics emerge that bolt-on software can't match. Helsing can specify some particularities for what the AI actually needs, rather than retrofitting intelligence onto platforms built for human pilots. The only way forwards for Helsing from this point is up and to the right.

Swarm Biotactics

Programmable cyborg insects for reconnaissance

Website: https://www.swarm-biotactics.com/

Founders & leadership: Stefan Wilhelm, Moritz Strube

Tags: bio-robotics; surveillance; sensors

YoF: 2024

Based in: Kassel, Germany

Notable backers: Vertex Ventures US, Possible Ventures

What Swarm Biotactics does

Although not personally someone you could call a huge fan of fist-sized deafening cockroaches, Swarm Biotactics makes the case anyway.

They build cyborg cockroaches, using Madagascar hissing cockroaches as the locomotion platform, attaching ultra-lightweight modular electronic backpacks that combine neural stimulation, sensors, and secure communications. The roach carries up to three grams of payload and navigates rubble, tunnels, and collapsed structures. A swarm of them becomes a real-time reconnaissance mesh in places conventional drones and ground robots cannot reach. By allowing them to work together to map, sense, and transmit real-time data, operators are provided high-density surveillance at a low cost.

Swarm is also moving pretty fast: founded in 2024, €3 million pre-seed, then €10 million seed in June 2025. By February 2026, more than forty engineers across Germany and a San Francisco subsidiary, with paying NATO customers including the Bundeswehr, and field validation completed in European and US operational environments. Wilhelm’s framing in the February announcement: “One year ago, this didn’t exist. Today, we deploy programmable cyborg insect swarms, field-tested and operational with paying NATO customers.” His other line: “No other company in the Western world is building this.”

The company’s total funding is now €13 million, with backing from Vertex Ventures US, Possible Ventures, and Capnamic.

Why it is fascinating

It is the most science-fiction company on the list. The premise reads like Black Mirror, but the company has gone from concept to NATO deployment in under two years. The closest historical analogue is DARPA's HI-MEMS programme from the late 2000s, which never produced operational systems. Swarm already did, in a third of the time, on private capital, out of Kassel.

Clear problem to solution pathway, and real dual-use cases. The same insect platform serves disaster response, humanitarian operations, and reconnaissance. Collapsed buildings and hazardous interiors are the same problem whether you're searching for survivors or scouting an adversary.

Aquark Technologies

Quantum sensing for a world with spoofed GPS

Website: https://www.aquarktechnologies.com/

Founders & leadership: Dr Andrei Dragomir, Dr Alexander Jantzen

Tags: quantum sensing; PNT; critical infrastructure

YoF: 2021

Based in: Southampton, UK

Notable backers: NATO Innovation Fund, EIFO, UKI2S (Future Planet Capital), MBDA, DIANA

What Aquark does

Aquark miniaturises cold-atom quantum sensors to the size of a matchbox. In plain English, it is a technology that can help critical systems know where they are, what time it is, or what is happening around them when satellite signals are jammed, spoofed, degraded, or unavailable.

The technology is based on more than sixteen years of research at the University of Southampton in vacuum engineering, microfabrication, and laser cooling. Their proprietary, patented laser-cooling method, called supermolasses, removes the need for an applied magnetic field, which collapses the size, weight, power consumption, and cost of every device the technology touches. The product line currently includes AQlock (a GNSS-independent atomic clock), AQuest (a portable cold atom source for researchers), and AQurate (a laser spectroscopy module).

The deployments are pretty impressive. In October 2024, Aquark trialled its cold atom system on the Royal Navy’s HMS Pursuer, capturing cold atoms continuously throughout testing. In April 2025, they ran the world’s first underwater cold-atom quantum sensor trial aboard the National Oceanography Centre’s Boaty McBoatface submersible (yes, a real name for an autonomous underwater vehicle (AUV) operated by the UK's NOC).

NATO Innovation Fund invested in Aquark in 2024 as part of a €5 million seed round, alongside EIFO, UKI2S, and MBDA, making it NIF’s first investment in a DIANA cohort company and its first quantum technology investment.

Why it is fascinating

It attacks one of modern warfare’s unsung dependencies. Russia jams GPS routinely across the Baltic and Black Sea, and civilian aircraft have already been affected. Every assumption in modern navigation, timing, and logistics depends on a satellite signal that adversaries have learned to disrupt cheaply. Aquark is uniquely positioned to bring a powerful solution.

Deep-tech founders successfully applying technology in the real world. Dragomir and Jantzen spun out of Southampton with patents on their unique technology. Moving cold-atom sensors from controlled labs to real-world environments is generally considered the biggest obstacle for commercializing quantum technology. Aquark has now demonstrated the ability to do so by deploying it on a Royal Navy vessel, on a drone, and underwater.

Finally, the database!

You can access the full database for free by clicking here. Feel free to share it and save it. Suggestions for additions or improvements are more than welcome as we plan to keep this a live database; you can send them either by responding to this e-mail or by texting me on LinkedIn.

thanks for sharing this. This info is really helpful.

Great note, Roko. In line with your thinking, we believe Europe is on the cusp of a market regime change in pursuit of greater strategic autonomy, energy resilience and stronger supply chains. This fiscal push has the potential to power its next wave of expansion, provided it can source the capital for it.

Defence spending is just the beginning, and we’ve mocked up a couple of notes that outline the investment implications for the ramp up in spending and would love to get your views on them. We are also in the midst of initiating coverage on investable opportunities in the space on the public side. Let us know if you would like to collaborate.

https://eosr.substack.com/p/european-defence-how-much-upside